Now more than ever, business operators should have a plan in place to manage during uncertain times. Even if your business is not directly impacted, it’s likely your customers, your supply chain, and your workforce will be to some extent.

So, how do you plan for uncertainty when every assumption is subject to change?

Now more than ever, business operators should have a plan in place to manage during uncertain times. Even if your business is not directly impacted, it’s likely your customers, your supply chain, and your workforce will be to some extent.

So, how do you plan for uncertainty when every assumption is subject to change?

Understand where you stand now

Businesses fail (or fail to thrive) for a myriad of reasons, but the precursor is often a failure to understand what is occurring and what to monitor. Strategically, managers need to be on top of their numbers to identify and manage problems before they get out of hand. If you do not know what the key drivers of your business are – the things that make the difference between doing well and going under – then it’s time to find out.

Understanding your cost structure and your breakeven point

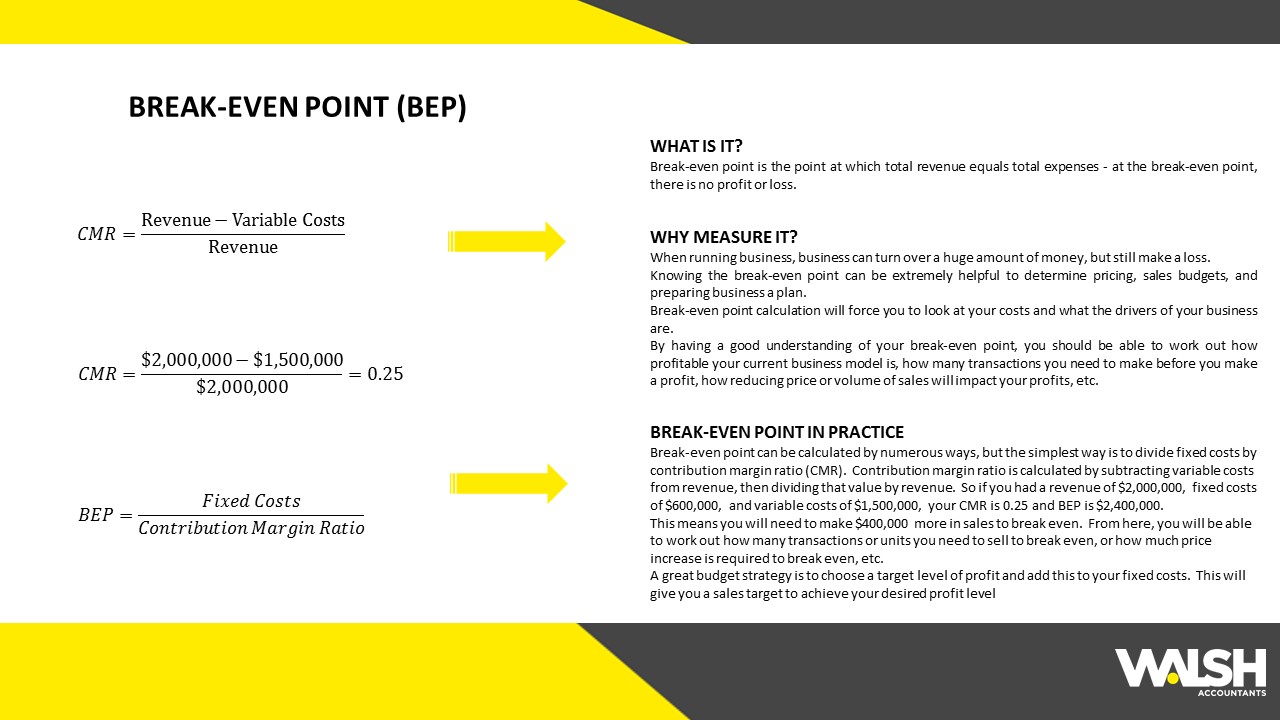

Do you know what your real cost of doing business is? Break-even point is the point at which total revenue equals total expenses – at the break-even point, there is no profit or loss.

Calculate your breakeven point by dividing your fixed expenses by your gross profit margin. This figure represents the level of sales income you need to breakeven.

Click HERE to download your own copy of the Break-Even Point KPI

Understanding your break-even point is crucial particularly when supply chains are impacted.

Not only will your break-even point assist you to monitor business performance, it’s critical when deciding whether or not to offer a discount. If your break-even point is well below your current operating level then you have a good buffer in your profits to manage growth, invest in further capital opportunities, and to protect yourself against further downturns in operating performance.

Understanding your KPI’s and Key Metrics

A Key Performance Indicator is a measurable value that demonstrates how effectively a company is operating and achieving key business objectives. KPI’s and Key Metrics should be used by every business as they use real time financial data to help understand past and current performance to help manage and drive the business.

The KPI’s and Key Metrics that you measure will vary depending on the industry in which you operate. The Walsh Accountants Focus Advisory Team have analysed a multitude of different industries and put together industry packs which include the key metrics we believe anyone operating in those industry should be tracking.

If you are interested in receiving a copy of your industry pack, please submit your details below and we will be happy to email them to you.

Plan, review, and adjust your budget

Your budget should be your best estimate of what is likely to occur based on current knowledge. To manage change, you can scenario plan where your budget forms the baseline, but you also forecast best and worst case scenarios based on potential risks and their likelihood (for example, the impact of another lockdown). Or, the simplest method is to use your budget as a baseline and regularly review and adjust depending on current conditions.

The greatest risk to your profit is unlikely to come from your cost structure. It is more likely to be revenue volatility. Keep your eye on your cost structure and make sensible cuts where appropriate. But, in your search for savings don’t remove your essential revenue generating capacity that you need.

If you would like to prepare a budget and cashflow projection for your business, we have made available some simple budget and cashflow templates you are welcome to use.

If you need some assistance preparing a budget and cashflow projection, either your accountant or a member of our Focus Advisory Team will be happy to assist you.

Lack of profit will erode your business – no cash will kill it!

A lack of profit will eventually erode your business, but not enough cash will kill it stone dead. Businesses will fail because they don’t manage their cash position. Plan, track and measure your cashflow. This not only means closely monitoring your debtor collections and inventory but also running a rolling three month cashflow position. This should provide an early warning of brewing problems.

Manage your debt levels carefully (your bank is likely to). While there is nothing wrong with debt, it is likely that the banks will be closely watching customer accounts. Where you have loan facilities in place make sure that you understand the loan terms and any debt covenants that you have entered into. These covenants could include regular reporting to the bank, debtor and working capital ratios, or debt to equity ratios. Where the banks may have been more relaxed about these in the past, this year will be different. If you believe that you need additional funding, talk to your bank early and don’t wait until the last minute. You’ll need to present your case on why you need it, how much, for how long and when it will be repaid.

Cash flows, operating budgets, cost control and debt management all need to be part of your business management. The more in control you are the lower your risk position.